A family member recently tore his patella and will be out of work for at least four months. He was upbeat about being out of work until his job fired him (business decision, not performance), and he learned he had long-term, not short-term, disability. Higher gas prices, inflation, and unemployment rates, and his injury have me thinking about wealth.

Today marks 164 years since the federal government initiated the largest wealth transfer in U.S. history. The Homestead Act of 1862 transferred 270 million acres acquired through the systematic dispossession of Indigenous lands to white males, an event often framed as a democratic distribution of wealth. This was not a democratic transfer. It was the confiscation of land for wealth creation.

I continue with what I love about these United States: how often the hypocrisy is written directly into the law. The Homestead Act of 1862 is an example. It promised 160 acres of “free land” to “any person” willing to claim and work it. But the land was not “free” or available to any person. The Act restricted access to the land through the definitions of “head of household” and “citizen” to establish a patrilineal wealth-building infrastructure designed almost exclusively for white men.

The Act was passed in 1862, three years before the abolition of slavery, so Blacks, likely willing to work it, were not eligible to claim the land. The Indigenous, who already had a claim and worked it, were not eligible to be citizens and stake a claim under the Act. Asians were not eligible to be citizens and stake a claim under the Act.

For white women, this exclusion was based on coverture. Married women had no independent legal identity—they were barred from owning property or entering into contracts, making them ineligible to claim Homestead land. Mississippi’s 1839 Married Women’s Property Act specifically protected a white wife’s ownership of enslaved Black people but did not remove other financial restrictions. It would be another 135 years before the Equal Credit Opportunity Act of 1974 required lenders to issue credit based on independent income, allowing women to be economic agents and engage in wealth creation.

This westward expansion actively eroded the established land wealth of Hispanic women. Their independent property rights under Mexican law were dismantled as the U.S. imposed its own property and coverture laws after the Treaty of Guadalupe Hidalgo.

That initial 160-acre stake was generational seed capital that could be farmed, borrowed against, or passed down. A rough estimate of the value of this transfer, using the $1.25-per-acre buyout price, is $337.5 million in 1862 dollars. Ignoring resource extraction (pricing barren land the same as acres sitting on timber, oil, or gold), commercial and residential real estate development, and land appreciation, the inflation-adjusted value of the land is $10.5 billion—a lower bound. This simple inflation calculation illustrates how the Homestead Act, a federal wealth transfer, helps explain why white male-headed households hold a disproportionate share of U.S. wealth today.

Compounding Intra-Gender Disparities

Black female-headed households had a median net worth of $13,600, and Hispanic female-headed households had a median net worth of $13,800 (see Figure 1). These women occupy the floor of the U.S. wealth distribution. Other women had a median net worth of $30,800, and White women had $86,621.

Figure 1. Median Net Worth by Ethnicity, Race, and Sex: 2022

Note: In the SCF data, the “Other” category is a residual grouping that includes respondents who identify as Asian, American Indian, Alaska Native, Native Hawaiian, Pacific Islander, other race, and multiracial. Source: Calculations by the Women’s Institute for Science, Equity, and Race, using the 2022 Survey of Consumer Finance, accessed via https://sda.berkeley.edu/.

The position of White women is often treated as the policy baseline for gender equity analysis. It should not be. A White female-centered gender analysis obscures the fact that White women ($86,621) sit in the middle of this distribution—above Black, Hispanic, and Other women, but below non-White men. Black and Hispanic women have 1/6 the net worth of White women, which is less than the net worth ratio for White women compared to White men, which is 1/4.

Additionally, Black and Hispanic men ($97,480 and $101,100) hold roughly 7 times the median wealth of Black and Hispanic women. The intra-racial gender gap is as large as the racial gap. Policy analysis that does not disaggregate at the intersection of race and sex obscures net worth inequality between men and women and within sex, missing this structure entirely.

Marital Status and Wealth Structure

Disaggregating by marital status exposes differences in how wealth accumulates across groups (see Figure 2). Married Black female-headed households have a median net worth of $196,200, 3.3 times the $58,780 held by married White female-headed households. Marriage is associated with substantially higher wealth for Black women than for White women when the comparison is within marital status. However, the overall Black female median is $13,600 because most Black female-headed households are not married, and unmarried Black female-headed households hold $12,500. The wealth distribution of Black women’s households is bimodal: a small married population with substantial wealth and a large unmarried population with near-zero wealth. Any policy targeting Black women’s wealth must address the asset position of unmarried Black women, which is where most Black women are.

Figure 2. Median Net Worth by Ethnicity, Race, Sex, and Marital Status: 2022

Note: In the SCF data, the “Other” category is a residual grouping that includes respondents who identify as Asian, American Indian, Alaska Native, Native Hawaiian, Pacific Islander, other race, and multiracial. Source: Calculations by the Women’s Institute for Science, Equity, and Race, using the 2022 Survey of Consumer Finance, accessed via https://sda.berkeley.edu/.

Married Hispanic female-headed households hold $11,000, the lowest of any married group, lower than unmarried White women ($86,621) and lower than unmarried Black men ($25,640). Marriage does not function as a wealth mechanism for Hispanic women. Unmarried Hispanic female-headed households hold $13,800, marginally higher than those of married households. Neither marital state produces meaningful asset accumulation. Unmarried White female-headed households hold $86,621 in wealth, more than married White female-headed households, which hold $58,780. An unmarried White male-headed household holds $114,230 in wealth, more than a married White female-headed household, which holds $58,780. The baseline wealth advantage of White men does not require marriage to exceed the married baseline of White women.

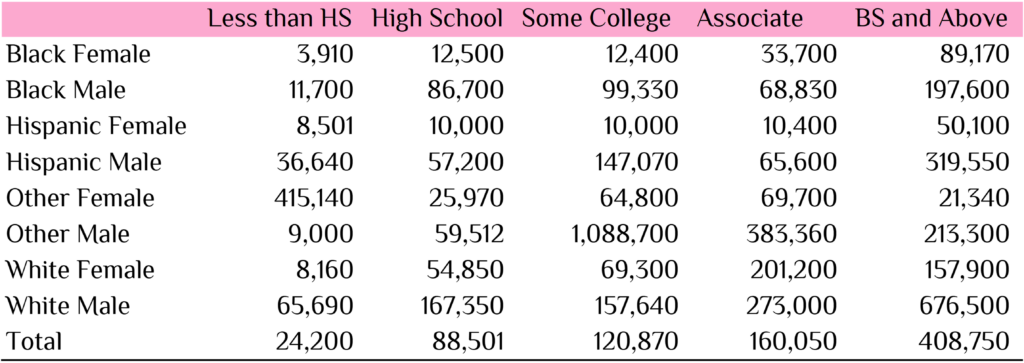

Education and Wealth Returns

Disaggregating by education demonstrates that education does not close the wealth gap (see Figure 3). It produces different returns for different groups at every level, and the absolute gap widens at higher education. Black women’s median net worth is essentially flat from high school ($12,500) through some college ($12,400). The associate degree produces a modest increase to $33,700. The bachelor’s degree or higher reaches $89,170, the first education level at which Black women accumulate meaningful wealth. The full return to a bachelor’s degree for a Black woman is $76,670 in additional median wealth over high school. For a White man with a bachelor’s degree or above, the median wealth is $676,500.

Figure 3. Median Net Worth by Ethnicity, Race, Sex, and Educational Attainment: 2022

Hispanic women’s education-wealth gradient is nearly flat through the associate degree level. High school, some college, and associate degrees all produce median wealth within the range of $10,000 to $10,400. A bachelor’s degree or above reaches $50,100. White women with an associate degree had a median wealth of $201,200, higher than that of those with a bachelor’s degree or above, at $157,900. The bachelor’s degree-or-above figure of $157,900 is 1.8 times the wealth of Black women with the same credential.

At the bachelor’s degree or above level, White male-headed households hold $676,500, and Hispanic female-headed households hold $50,100, a ratio of 13.5:1. At the less-than-high-school level, White male-headed households hold $65,690, and Hispanic female-headed households hold $8,501, a ratio of 7.7:1. More education produces a larger absolute gap, not a smaller one.

In the Red

Single Black women with children carry a negative net worth at 36.4 percent. Black female-headed households carry negative net worth at a rate of 25.6 percent, the highest group rate in the sample, driven primarily by single Black women with children (see Figure 4). The wealth structure for Black women centers on single households, which carry debt at rates unmatched by other groups.

Figure 4. Negative Net Worth Rates by Household Composition: 2022

Hispanic female-headed households carry negative net worth at a rate of 17.8 percent. Married Hispanic women with children carry a negative net worth at 34.3 percent, nearly double the rate for single Hispanic women with children at 16.4 percent. For Hispanic women, marriage combined with children correlates with greater financial precarity, not less. The aggregate group percentage conceals this inversion.

White female-headed households carry a negative net worth at a rate of 14.0 percent. Married White women without children carry a negative net worth at 36.5 percent, the highest single cell rate across all groups. Single White women with children carry a negative net worth at 15.9 percent, and married White women with children carry a negative net worth at 15.9 percent. The gender wealth gap between White women and White men is 9.6 percentage points (14.0 percent minus 4.4 percent).

Single-headed households with children carry a negative net worth at 18.1 percent across all groups. Married households with children carry a negative net worth of 5.1 percent. The exception is married Hispanic women with children, who have a negative net worth of 34.3 percent, reversing the standard pattern. White male-headed households carry a negative net worth at 4.4 percent, the lowest group rate.

The Homestead Act established a wealth distribution that 164 years later remains visible in household balance sheets. White male-headed households have the lowest negative net worth rate at 4.4 percent and the highest median wealth across all education and marital status categories. Black and Hispanic women occupy the opposite end: median wealth below $14,000, negative net worth rates exceeding 25 percent for Black women and 17 percent for Hispanic women, and returns to education and marriage that do not function as wealth-building mechanisms. Disaggregation reveals that policy interventions designed around aggregate gender gaps or racial gaps will miss that inequality operates at the intersection of race and sex, and the mechanisms that build wealth for one group—marriage, education, homeownership—do not operate uniformly across groups. Policies that fail to account for these differences will reproduce the inequalities they claim to address.

Rhonda V. Sharpe is the president and founder of the Women’s Institute for Science, Equity and Race. Her research focuses on gender and racial inequality, the diversity of STEM, and the demography of higher education.